Topical at the moment is the use of hydrogen as the fuel of the future. Toyota has launched its second-generation hydrogen car, the Mirai. Prime Minister Scott Morrison is putting a political spin on Australia having a Hydrogen Valley.

Twiggy Forrest is in the news every second day announcing a breakthrough for the production of hydrogen, or the next purchase of an ammonia plant for Fortescue Future Industries. The Weekend Australian contained an article about hydrogen and FFI. All the above was enough to pique my interest and subsequently investigate whether hydrogen was a viable alternative to fossil fuels or lithium batteries, and whether WA’s tenure legislation is ready for the Hydrogen Valley.

Nearly all hydrogen used is for refining petroleum, treating metals, producing fertilizer and processing foods; however, there will be an expanding market for green hydrogen.

Japan currently imports fossil fuels for 94% of primary energy supply and they want to cut emissions by 26% by 2030 and 80% by 2050. South Korea is in the same boat, they import 81% of energy as fossil fuels.

Hydrogen is produced by several different methods. Currently, 96% of hydrogen is made with fossil fuels; this produces 830 million tonnes of CO2 a year, the equivalent of the entire production of CO2 by Britain and Indonesia combined.

50% of hydrogen is produced by steam reforming of natural gas to temperatures in excess of 1000 degrees Celsius, this is known as “grey hydrogen”. Another 46% is produced by coal or oil.

Only 4% of hydrogen is produced by electrolysis splitting the water atom into hydrogen and oxygen (Refer to this video that explains it in plain English), this use of renewal energy is commonly referred to as “green hydrogen”.

The production of hydrogen is only between 60% to 80% efficient, this depends on what sources you read. A recent announcement in March 2022 by the University of Wollongong and ARC Centre of Excellence for Electromaterial Science stated they have developed new electrolyser technology that is 98% efficient.

To transport hydrogen, it can be either frozen to -253 degrees Celsius (30% of the cost of making hydrogen), compressed to 70 mega pascals (700 times normal atmospheric pressure) or converted to ammonia which can be stored at ambient pressures (90% of ammonia is used as fertilizer for agriculture).

The energy content of 1 kg of hydrogen is 33.33 kwh which equals about 4 litres of petrol.

Buying hydrogen in Perth at the moment is an administrative nightmare, you can’t just rock up to a service station and fill up, although Woodside has stated it will build a Hydrogen Highway in WA in the near future.

The prices quoted for hydrogen have been between $3 and $8 per kilo. The purchase price from Supagas, Perth’s only hydrogen supplier, was not disclosed. For the hydrogen to be competitive the production cost needs to be $1.50 per kg.

Given that the well-to-wheels efficiency of charging an onboard battery and then discharging it to run an electric motor in a PHEV or EV is 80% (four times more efficient than current hydrogen fuel cell vehicle pathways), I won’t be rushing out to buy the Toyota Mirai just yet.

In October 2021, Woodside announced the building of a hydrogen plant in Kwinana WA. This will obtain 500,000 tonnes of hydrogen from gas annually, using both the steam reforming and electrolysis methods, with all CO2 emissions abated. The Conservation Council of WA called this is a green washing exercise.

FMG was also highly critical of Woodside’s hydrogen production stating “The oil and gas sector are using the colours of the rainbow to call it clean hydrogen, but by it being made from fossil fuels, it is anything but”.

The largest problem with the production of green hydrogen is securing the land. Woodside can use the Petroleum and Geothermal Energy Resources Act 1967 (PGERA) to overcome this obstacle.

Under the PGERA, petroleum operations are any operation for the extraction and processing of ‘petroleum’ which is defined as naturally occurring hydrocarbons in a gas, liquid or solid state. This then encompasses the extraction of hydrogen from gas.

The Mining Act 1978 cannot be used as the definition of ‘mining operations’ include any method to obtain a mineral, including from the sea or water and “all acts …conducive to such operation or purposes”

Under natural conditions hydrogen is a chemical element and a gas, not a solid. As a result, hydrogen cannot be considered a mineral and the extraction does not fall within the purview of the Mining Act 1978.

Fortescue Future Industries (FFI), a subsidiary of FMG, plans to produce 15 million tonnes of green hydrogen a year. In October 2021, Mr. Forrest said he wanted to make his first big hydrogen investment in WA, but the State’s red tape was holding FFI up.

To produce FFI’s proposed hydrogen would require the erection of either 10,000 km² of solar panels or 190 giant wind turbines. It takes 9 litres of purified water to produce every kilo of green hydrogen. That’s 13.5 gigalitres for 15M tonnes of green hydrogen meaning a substantial water purifying and storage facility would be required.

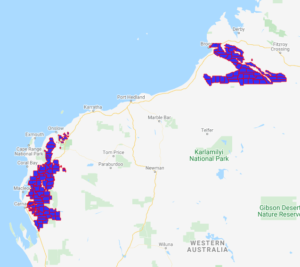

FFI could purchase freehold land to develop hydrogen. Though, it appears that they have applied for 138 exploration licences covering an area the size of Croatia, approximately 56,000 km², near Broome and Carnarvon. This is presumably for solar and wind farms (refer to the map below). The area around Broome is on unallocated crown land and the area between Carnarvon and Exmouth is on pastoral leases.

As demonstrated above, exploration licences cannot be used to secure land for hydrogen production.

The State Government appears to have reached the same conclusion. Dr. Tony Buti, a Minister for the WA State government, on the 15 December 2021 announced the release of three million hectares of unallocated crown land for private investment in carbon farming to aid climate change mitigation.

“Proposed carbon farming areas will be able to take advantage of the new flexible form of land tenure known as a ‘diversification lease’…”

The proposed Diversification Leases (DL), under the Land Administration Act 1997 and the Public Works Act 1902 (WA), are currently proposed to allow proponents to develop the wind and solar farms required for hydrogen production, carbon farming, horticulture projects, and preservation/rehabilitation biodiversity.

A DL can be granted over a pastoral lease, the pastoral leaseholder needs to surrender that portion of the lease. The pastoral leaseholder is not compelled to surrender their tenure.

I suggest it would be a time-consuming process negotiating with pastoral leaseholders to sell their land for the DL, having it surveyed and then getting Landgate to re-categorise it. With an 18-month waiting list for the surveying of a mining lease, the survey of a DL is not for the impatient. One must account for Landgate’s snail pace of title changes along with the Office of State Revenues processing of Stamp Duty; the processing time would be considerable.

It is proposed that a Diversification Lease can co-exist with mining tenements.

I suggest it would be an advantage if hydrogen production operated under the Mining Act as the tenure would be easily adapted.

For example, Miscellaneous Licences can coexist with pastoral leases and other mining tenements. Miscellaneous Licences already have native title processes in existence and precedence in law. DLs are a new type of tenure with no existent Native Title precedent.

I can’t imagine the possibility of a greater disaster than allowing private industry and Landgate to manage hydrogen generation through use of diversification leases. One only has to refer to the incident in Lebanon in August 2020 as an example of what possible could occur.

This sentiment is heightened as there is an alternative Government Department platform, already in existence, with tenure processes, Occupational Health and Safety laws, regulations and processes to safely manage a highly combustible gas. A few tweaks to the Mining Act could encompass hydrogen production.

Mr. Forrest was of the opinion the State’s red tape was holding FFI up, and in the manifestation of WA Government’s inaction, FMG took its business to Queensland. It was announced in October that FMG was setting up a hydrogen electrolyser in Gladstone. Gladstone is the epicentre of industry in QLD with high carbon producing industries including aluminium smelters, a cement plant, and an ammonium nitrate plant; all powered by coal-driven power stations.

The location on the green energy supply was announced in Aldoga and it appears that Queensland’s Mineral Resources Act 1989 has a wider definition of mineral that includes the extraction of hydrogen from water using electrolysis.

The newly registered Within Energy Pty Ltd, wholly owned by Mimo Strategies Pty Ltd (controlled by Jane Whiddon of Perth’s western suburbs), applied for an Exploration Permit for Geothermal Energy on the 18th of November 2021. The permit is conveniently in and around Gladstone making it even more difficult for FFI to produce and use renewable energy. How coincidental is that?

While waiting for the WA government to legislate tenure for hydrogen production, perhaps FFI could establish a small sand or clay mine near Carnarvon, the windiest town in WA, and use miscellaneous licences to erect renewable energy facilities. This is allowed under r42B of the Mining Regulations that permits ‘power generation and transmission facilities’ and ‘water generation facilities’.

Considering the number of hurdles a hydrogen producer faces securing tenure to develop the so-called Hydrogen Valley, and the value it is to WA, the State Government should provide more realistic assistance to provide land and simplify the legislation around hydrogen production development.

LandTrack Systems holds a number of training courses that assist people in managing their tenure:

Understanding Tenement Expenditure

Navigating Exploration Agreements